Welcome to the realm of 2/1 buydown calculators, where dreams of homeownership take flight. This comprehensive tool empowers you to envision a future with reduced monthly mortgage payments, paving the way for financial freedom and the realization of your aspirations.

Immerse yourself in the intricate details of 2/1 buydowns, unraveling their mechanics and uncovering the secrets to unlocking substantial savings. With each calculation, you’ll gain invaluable insights, enabling you to make informed decisions that align with your financial goals.

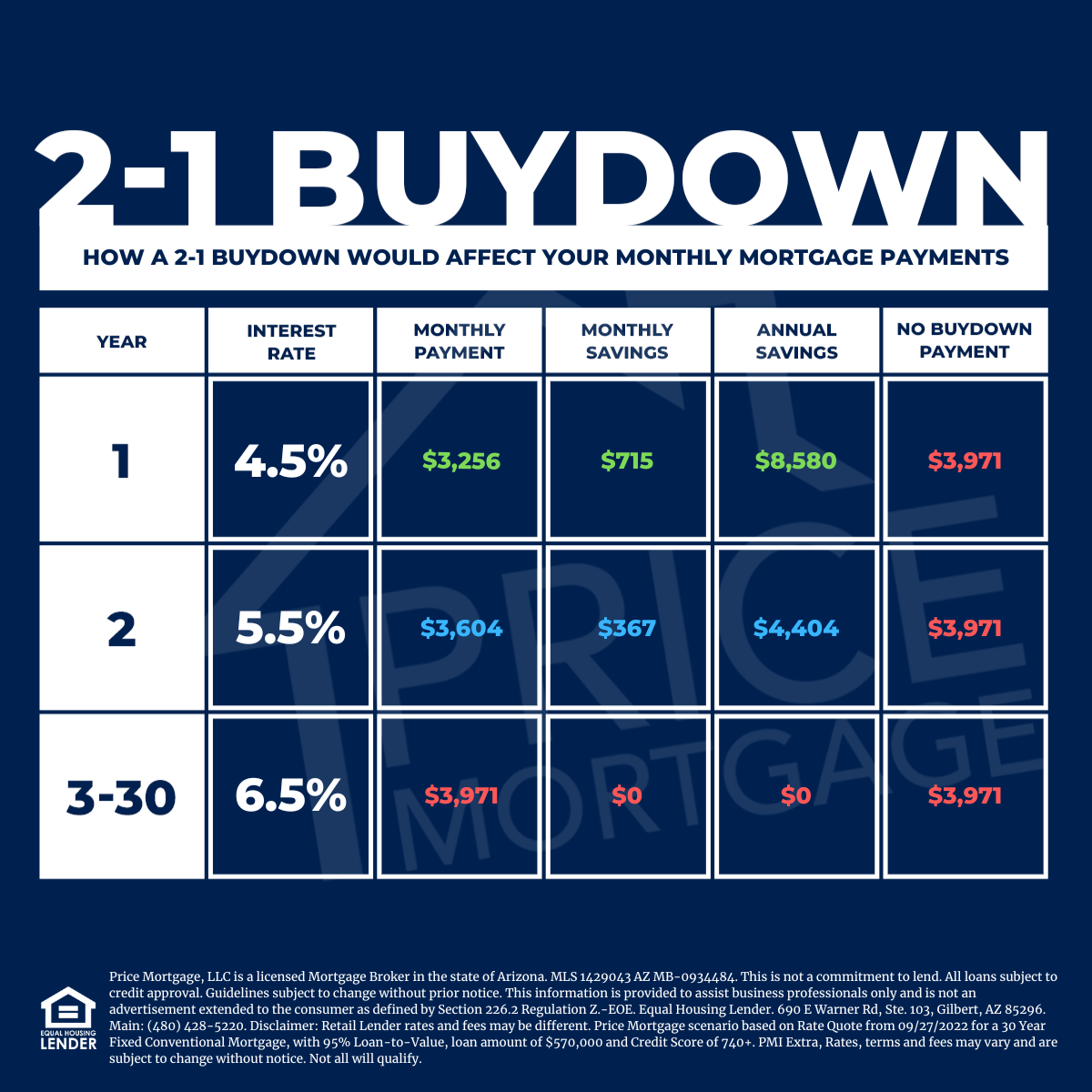

2/1 Buydown Basics

A 2/1 buydown is a type of mortgage assistance program that helps homebuyers lower their interest rates for the first two years of their loan. This can make it easier to qualify for a mortgage and save money on monthly payments.

Here’s how a 2/1 buydown works:

- In the first year of the loan, the interest rate is reduced by 2%.

- In the second year of the loan, the interest rate is reduced by 1%.

- In the third year of the loan, the interest rate returns to the original rate.

Benefits of a 2/1 Buydown

There are several benefits to using a 2/1 buydown, including:

- Lower monthly payments:The reduced interest rate can save you money on your monthly mortgage payments, making it easier to budget and afford your home.

- Easier to qualify for a mortgage:The lower interest rate can help you qualify for a larger loan amount or a lower down payment.

- More flexibility:A 2/1 buydown can give you more flexibility in your budget, allowing you to save for other financial goals or make unexpected expenses.

2/1 Buydown Calculations

Calculating the monthly payment with a 2/1 buydown involves a specific formula that takes into account the loan amount, interest rate, and the duration of the buydown period.

Monthly Payment Formula

Monthly Payment = (Loan Amount x Interest Rate x (1

- Buydown Percentage)) / (1

- (1 + Interest Rate)^(-Loan Term in Months))

Eligibility for 2/1 Buydowns

To qualify for a 2/1 buydown, you must meet certain eligibility criteria. These criteria may vary depending on the lender and the specific loan program, but there are some general requirements that apply to most 2/1 buydowns.

First, you must have a good credit score. Lenders typically require a credit score of at least 620 to qualify for a 2/1 buydown. You must also have a stable income and a debt-to-income ratio that meets the lender’s requirements.

Loan Types

Not all types of loans qualify for a 2/1 buydown. The most common types of loans that qualify are conventional loans and FHA loans. VA loans and USDA loans do not typically offer 2/1 buydowns.

Restrictions and Limitations

There are some restrictions and limitations on using a 2/1 buydown. For example, you may not be able to use a 2/1 buydown if you are purchasing a second home or an investment property. You may also be required to pay a higher interest rate on your loan after the buydown period ends.

Comparison to Other Buydown Options: 2/1 Buydown Calculator

A 2/1 buydown is not the only type of buydown option available. Other common options include 3/2 buydowns and 1/0 buydowns. Each type of buydown has its own unique advantages and disadvantages, and the best option for you will depend on your individual circumstances.

3/2 Buydowns

A 3/2 buydown is similar to a 2/1 buydown, but it provides a larger initial interest rate reduction. With a 3/2 buydown, your interest rate will be reduced by 3% during the first year and 2% during the second year.

This can result in significant savings on your monthly mortgage payments, especially if you have a high-interest rate loan.

However, 3/2 buydowns typically come with higher upfront costs than 2/1 buydowns. This is because the lender is taking on more risk by providing a larger initial interest rate reduction.

1/0 Buydowns

A 1/0 buydown is a less common type of buydown that provides a smaller initial interest rate reduction. With a 1/0 buydown, your interest rate will be reduced by 1% during the first year only. This can result in some savings on your monthly mortgage payments, but it is not as significant as the savings you would get with a 2/1 or 3/2 buydown.

1/0 buydowns typically come with lower upfront costs than 2/1 or 3/2 buydowns. This is because the lender is taking on less risk by providing a smaller initial interest rate reduction.

Summary of Key Differences, 2/1 buydown calculator

The following table summarizes the key differences between 2/1 buydowns, 3/2 buydowns, and 1/0 buydowns:

| Buydown Type | Initial Interest Rate Reduction | Upfront Costs |

|---|---|---|

| 2/1 Buydown | 2% for the first year, 1% for the second year | Moderate |

| 3/2 Buydown | 3% for the first year, 2% for the second year | High |

| 1/0 Buydown | 1% for the first year only | Low |

Concluding Remarks

As you conclude your journey through the world of 2/1 buydown calculators, remember that knowledge is the key to unlocking the doors of opportunity. Embrace the power of this tool, and let it guide you towards a future filled with financial stability and the unwavering joy of homeownership.